Question 1

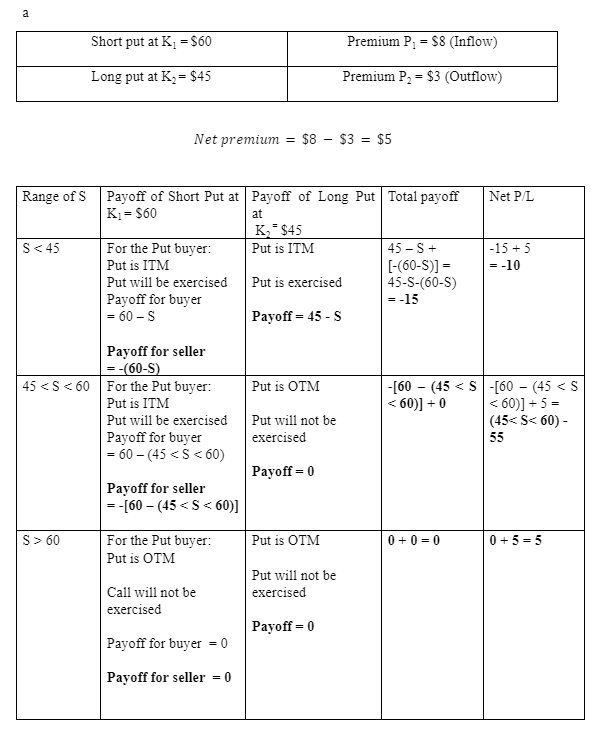

An investor writes a put option with exercise (strike) price of $60 and buys a put with exercise price of $45. The puts sell for $8 and $3 respectively. If the options are on the same stock with the same expiration date,

A)

Calculate the payoff and profit/loss of this strategy.

B)

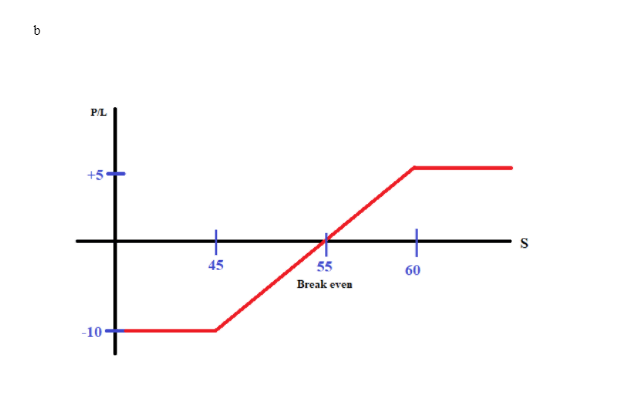

Draw the profit/loss diagrams for this above strategy at expiration date of options.

C)

Calculate the breakeven point for this strategy and discuss whether the investor is bullish or bearish on the underlying stock.

When the investor writes a put option with a strike price of $60 , $8 premium is received and there will be a negative payoff when the current stock price falls below $60. A long-put option will cost the investor $3 and have a positive payoff if the stock price falls below $45. In combining both contracts the investor will make a maximum profit of $5 per contract and a maximum loss of -$10 per contract. The breakeven point can be calculated with this formula Breakeven Point = Strike Price of Short Put (60) – Net Premium Received (5) or mathematically the breakeven point can also be seen here , -[60 – (45 < S < 60)] + 5 = (45< S< 60) – 55

The breakeven point is $55

The investor is utilizing an option strategy call a vertical bull put spread. A vertical spread consists of buying and selling an option contract simultaneously with different strike prices with the same expiration date. A bull put spread involves buying a put and selling a put at the same time. The strike price of the short put contract will be higher than the long-put contract.

The vertical bull put spread is a bullish strategy. This strategy suggest the investor is expecting a moderate rise in the underlying stock. The investor thinks the buyers of the put contracts will have a lower probability of exercising the stock. At the same time a lower strike long put is also bought as a form of insurance for the investor. This strategy pays a net premium which is an income made initially. The maximum loss that can be made is the difference between the strike price and net premium. This is capped and important to an investor as the maximum loss is known upfront. If the investor is wrong in his strategy he might suffer a huge loss if the stock price increases drastically, fortunately it is not a naked put and this strategy has an insurance which is the long put limiting his lost to only -$10 per contract. However, this is a double edge sword as profit is also capped, and the investor has to deal with it if the price of the underlying stock increases drastically.

Question 2

Determine the price of a European put option on a non-dividend-paying stock when the stock price is $655, the strike price is $720, the risk-free interest rate is 10% per annum, the volatility is 30% per annum, and the time to maturity is six months.

What is the price of a European put option in (a) if the stock pays dividends with a dividend yield of 6% per annum?